Prior Authorization

“The hunted news I get from some obscure patients’ eyes is not trivial. It is profound.”

William Carlos Williams (Autobiography, 1951, Ch. 54: “The Practice”)

Something actually has changed

The headlines are reassuring.

Long-term cancer survival rates continue to improve. Cardiovascular mortality continues to decline. Stroke outcomes continue to improve markedly. By 2023, more Americans were covered by health insurance than at any previous point in the country’s history.1 The Consumer Price Index shows healthcare inflation has been a manageable 2.8% annually over the past five years2.

And yet, healthcare is where many of us first notice that something has shifted.

Vera and I first noticed it with our third child’s delivery at Sibley, a Johns Hopkins hospital. But the same pattern repeated for me with a vasectomy at a Medstar health center a year later, then a first colonoscopy a year after that.

It took nine months to schedule a spot for a routine family planning procedure. It took four to schedule preventative care. With the colonoscopy, someone at Medstar said that there was no way to know in advance what it would cost me out-of-pocket.

Revenue Integrity

Hospitals are a place to receive care. But they are also an asset that converts inputs into financial outputs.

As a financial asset, hospitals define success through industry metrics like throughput and asset utilization.

Consider how the world looks to the CFO of a hospital system. Let’s call her Sarah. She isn’t optimizing these metrics to boost a stock price: a significant majority of US health systems are non-profits. Sarah’s fighting to keep the emergency department open.

She knows that 40% of U.S. hospitals are currently operating in the red. With operating margins around 1.5% and nurse labor costs up 27%, efficiency is what separates continued operation from closure.

To keep the doors open, Sarah relies on sophisticated software systems known as Revenue Cycle Management.

In a modern hospital, insurers do not pay for “care.” They pay for codes. Every distinct action—a checkup, a suture, a complex diagnosis—must be translated into a specific billing code to trigger payment. If a doctor notes “pneumonia” but fails to document the specific clinical indicators of “complex pneumonia with complications,” the hospital might lose thousands of dollars for the exact same treatment.

In 2015, the U.S. healthcare system adopted a new standard for codes. Overnight, billing codes expanded from roughly 14,000 to 68,000. The administrative burden of defining a “broken arm” fractured into half a dozen hyper-specific variations.

This explosion in granularity outpaced human cognition. Revenue Cycle Management became a technological arms race. Sarah invests millions in algorithms that scan medical notes in real-time, hunting for keywords that justify higher-severity codes.

The software nudges a “Level 3” office visit to a “Level 5” emergency response. It suggests adding a secondary diagnosis of “malnutrition” or “respiratory failure” to a standard admission. In the industry, this is called “Revenue Integrity.” To Sarah, it is the only way to capture the full value of the work her staff performs.

But revenue optimization alone cannot cover rising labor and drug costs. Sarah must also eliminate the buffer — the spare capacity that absorbs variation but generates no revenue.

Over time, the efficiency pressure Sarah manages compressed that buffer. Scheduling tightened toward full capacity. Staffing ratios thinned. Discharge timelines accelerated.

Buffer eroded slowly for decades. Then the shock arrived.

When the pandemic hit, the “lean staffing” models that worked on paper collapsed. Between 2020 and 2023, around 100,000 registered nurses left the profession3.

Staff already at their limit were asked to sustain the impossible. Many left. Institutional memory left with them. The physical beds remained, but without the staff to tend them, they became “ghost capacity,” or assets that exist on the ledger but cannot accept a patient.

Even with the pandemic behind us, the system has reshaped how we often experience care. Staffing gaps now stall admissions. Scheduling surges spill into hallways. Delayed discharges cascade through emergency departments.

Most of us don’t get sick or fall off a ladder on a predetermined schedule. Surgeries overrun. Discharges hinge on insurers, transportation, and home care availability. These are all inputs beyond hospital control. With buffers already thinned and the workforce shattered, that variation now converts directly into exposure for patients.

Slowly, Then All At Once

Operations science predicts this exactly. Kingman’s Formula describes how wait times behave under load—and the insight is unforgiving. As utilization approaches full capacity, delays don’t rise gradually. They rise exponentially.

A system running at 60% capacity absorbs variation easily. At 85%, delays grow quickly. At 98%, even minor disruptions—an absent nurse, a delayed discharge, a surge of arrivals—produce cascading backlogs, often paralyzing a system in seemingly inexplicable ways.

This is how breakdowns often happen: slowly, then all at once.

This phase change explains why the system hasn’t snapped back even as the consequences of the pandemic have faded. It is tempting to view this instability as a temporary labor cycle, a disruption that will smooth out as wages rise and new nurses graduate. But the same logic of optimization acts as a ratchet.

To pay for the 27% increase in labor costs without a matching increase in reimbursement, Sarah cannot afford to rebuild the buffer she lost. She must do the opposite: run the remaining assets at even higher utilization to cover the increased cost per unit.

We’re in a new equilibrium where the steep part of the exponential curve is the daily operating target.

“We are truly honored to be recognized with this high-performance award. While our tradition of clinical excellence dates back more than 85 years, our approach to revenue cycle could not be more contemporary. Our entire revenue cycle team is dedicated to making the financial experience a seamless one for our patients.” — Steven Sinclaur, CPA, CFO of Graves-Gilbert Clinic in 2023

Prior Authorization

But our experience of healthcare isn’t limited to health systems.

Insurers manage risk across millions of claims, using those same 68,000 codes. At that scale, human discretion inevitably gives way to automation. Algorithms process submissions, compare them against statistical norms, and route deviations into denial or appeal workflows.

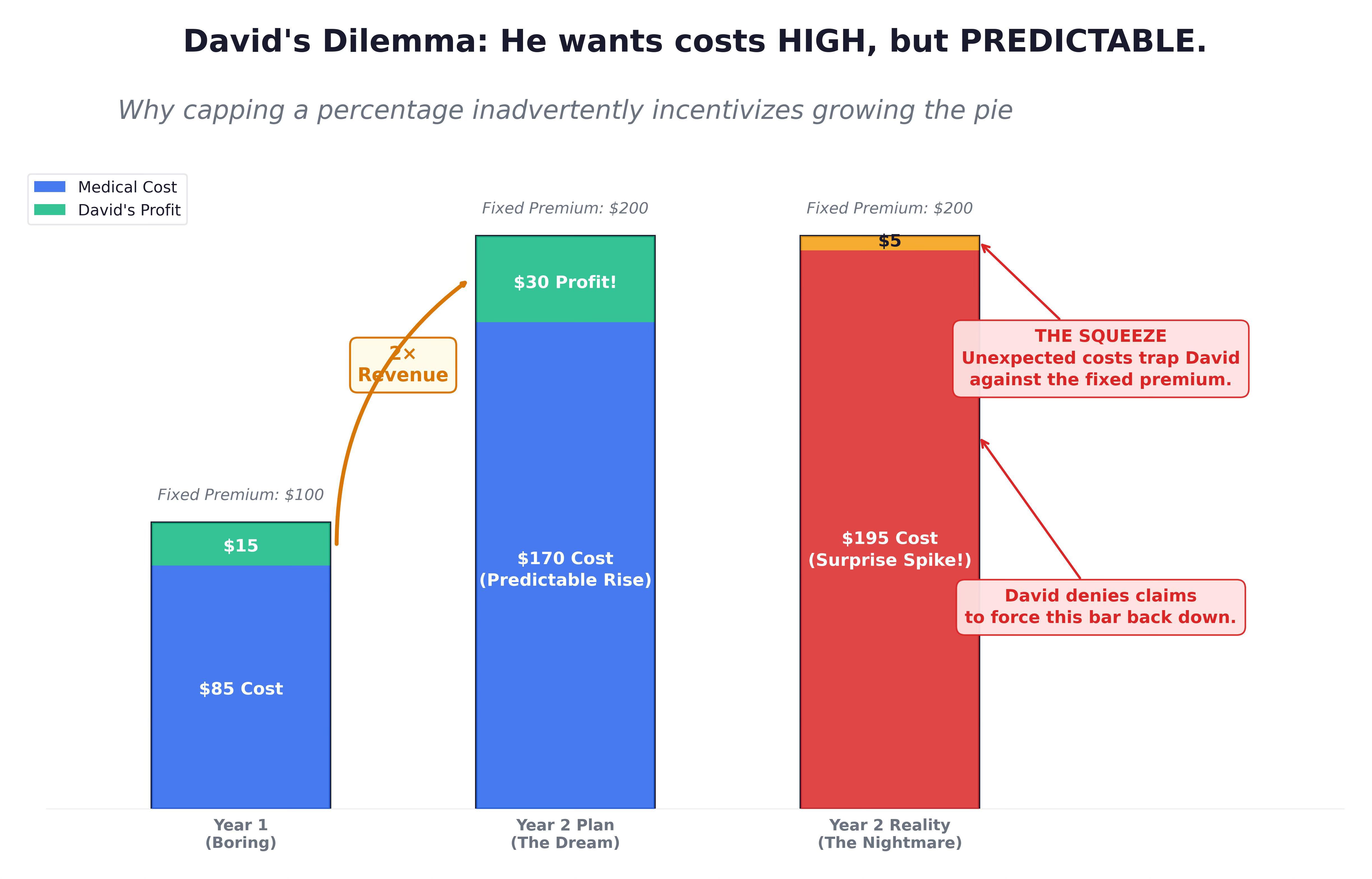

Consider how this looks to a VP of Claims Operations at a major insurer. We’ll call him David. He isn’t optimizing for affordability. He is optimizing for predictability.

When his algorithm flags a mismatch, David sees a guardrail against “waste” and “upcoding,” not a patient in distress. He optimizes to protect the risk pool while ensuring his shareholders maintain a competitive return on equity.

But David operates under a specific regulatory constraint that twists these incentives.

The Affordable Care Act caps David’s profit margin. Under the Medical Loss Ratio rule, 80 to 85 cents of every premium dollar must be spent on care. He can only keep the remaining 15 cents for administration and profit. If David successfully crushes the cost of care, his 15% slice shrinks in absolute dollars. If the cost of care rises, his 15% slice grows.

Mathematically, David wants his overhead to be lean. But he wants the cost of healthcare to rise—predictably.

David sets his premium rates 12 to 18 months in advance. If the hospital raises its prices faster than that schedule, David’s margin for the current year vanishes. This transforms the “Denial” from a medical decision into an algorithmic financial throttle.

Prior authorization governs utilization before care occurs. Claims adjudication evaluates billing afterward. David uses them to slow the hospital’s spending just enough to ensure it matches the premiums he has already collected.

The hospital submits the highest defensible price and moves on. The insurer adjudicates the low payment (or denial) and closes the file. Each system behaves logically within its own frame, effectively passing the mismatch to the other side.

Sheldon Ekirch was 28 and about to start her legal career when she was diagnosed with small fiber neuropathy, a condition causing near-constant pain. Her neurologist recommended a treatment. Anthem denied it as not medically necessary. She appealed; the state review upheld the denial. Her parents withdrew from their retirement savings to cover what her insurance would not. “I’m paying a lot of money for health insurance,” she said. “I don’t understand why they won’t help me.”4

What the Index Shows

Tom Contos, a healthcare consultant in Chicago, used Northwestern Memorial Hospital’s online cost estimator before his diagnostic colonoscopy in June 2024. His estimate: $2,381 out-of-pocket. He paid $1,000 upfront as the hospital requested.

The bill that arrived was $4,047.5 Northwestern had billed two colonoscopies — modifier codes for removing polyps in different ways. Its rate for the procedure was more than twice the Aetna median at other Chicago-area hospitals. The charge was, the hospital told him, “non-negotiable.”

“I said, ‘I don’t understand this,’” Contos recalled. “Then I started to research the cost.”

The Consumer Price Index captures what a basket of goods costs this month versus last month. It is designed for consistency of measurement. When a hospital updates its chargemaster, the index verifies that the defined service — the specific procedure code — remains consistent over time. Not whether the service was available. Not whether it worked.

In 2023, that methodology reported health insurance prices falling nearly 4%.6 It did not record whether you waited three hours in triage, or missed the window for an epidural, or received bills for uncovered services for years later.

The costs created by the throttle — the denied claims, the delayed approvals, the hours of unpaid coordination labor — are invisible to the index.

When Premiums Rise

An economist might argue that all this is a temporary disequilibrium: as scarcity bites, premiums will rise, reimbursements will follow, and hospitals will use that new capital to rebuild the workforce and restore the buffer.

This assumes that a dollar of new premium translates into a dollar of new capacity.

In healthcare, that transmission belt is broken.

As premiums rise, the additional revenue enters what healthcare advocates call a shooting war. David, the insurer, doesn’t use the surplus to loosen authorization rules. He invests in more sophisticated denial algorithms to protect the new, higher stakes.

Sarah, the CFO, doesn’t use a reimbursement hike to hire now “redundant” nurses for a rainy day. She uses it to pay the 27% wage premium for the staff she already has and to upgrade the RCM software needed to fight David’s new algorithms.

Inflation doesn’t buy capacity; it buys complexity. It makes it feel more arbitrary for you.

Robert Cano managed a retail store. Tiffany worked in bank compliance. Together they earned nearly $100,000 a year. Robert’s employer plan cost $500 a month. Their first child was born in January 2018 — healthy, no complications. The bills came to more than $12,000. Robert took on three additional jobs — substitute teaching, overnight security, delivering sandwiches for a fast-food chain 40 miles away where the tips were better — and sometimes worked 120 hours in a week.

“My husband is working four jobs. I work full time. We’re a hardworking family doing our best and not getting anywhere,” Tiffany said. “How does everybody else do it?”7

41% of American adults are asking the same question. Together they carry $88 billion in medical debt.8

Without a Profit Motive

Ervin Kanefsky was 94 when he fractured his shoulder in a fall. His doctor ordered him admitted as an inpatient. The hospital’s utilization review team overrode that order. At discharge, he was told he had been classified as an observation patient the entire time. Without three qualifying inpatient nights, Medicare would not cover his skilled nursing care. The bill: $9,145.

“If I had gone home, I would have died,” he said. “I tried every which way.”9

Observation status is a billing designation, not a clinical one. The hospital applies it based on Medicare’s payment rules, not a doctor’s judgment. Roney had been in a hospital bed for three days. The classification that determined his cost was invisible to him until the bill arrived.

The designation carries a second trap. Medicare covers skilled nursing and rehabilitation only after at least three consecutive inpatient nights. Observation nights don’t count. A patient hospitalized for a hip fracture — four days in a hospital bed, classified as observation — may find that Medicare covers none of the subsequent rehabilitation. Nursing home care averages $290 a day. A month of rehab a family assumed was covered can cost $8,000 or more.

In Medicaid and Medicare Advantage, the optimization can take a different form. Coverage exists on paper for those enrolled. But access does not always follow. Patients encounter ghost networks: clinics listed but unavailable, with appointments impossible to secure.

The Cash Market

Veterinary medicine operates largely as a cash market — no insurers, no prior authorization, no David. But the “Main Street” veterinary storefront is increasingly an illusion. Mars, the candy company, owns Banfield, VCA, and BluePearl. Together with one other private equity consolidator, corporate chains now control roughly 30% of general practices and nearly 75% of emergency clinics.

When Kathleen Whitman’s daughter’s dog swallowed a Kong toy, her local clinic’s x-rays suggested an intestinal obstruction. She was referred to a corporate emergency hospital. Before she had committed to anything, they handed her a clipboard in the waiting room. The number was $10,000. “I said, ‘No, I’m just coming in to hear the price,’” she recalled. She found an independent clinic — founded by two vets who had left Banfield and VCA — where the surgery cost significantly less.10

The other failure mode doesn’t involve prices at all. Jennifer Fraser’s new puppy Simba was straining to urinate and couldn’t. She called every emergency clinic in the Pittsburgh area. Every one gave her the same answer: unless her pet was dying, they couldn’t see him tonight. A urinary blockage — which looks exactly like a urinary tract infection — can be fatal within hours. She didn’t know which one she was looking at.11

The American Prospect documented why. At Mars-owned clinics, one technician now oversees 18 patients. The old standard was 6.12 When a single staff member calls out, the system has no buffer. The door doesn’t lock. The lights stay on. The sign still says 24-hour emergency care. The answer is still the same.

You

Eric Tennant was a safety inspector for the West Virginia Office of Miners’ Health and Safety when he was diagnosed with stage 4 bile duct cancer. His oncologist recommended a noninvasive procedure that might slow the progression. UnitedHealthcare denied it four times. The insurer reversed the denial after journalists contacted them for comment. Tennant had become too ill for the procedure by then. He died September 17, 2025.13

This is what arbitrary feels like: the outcomes you experience are defined by algorithms optimizing for someone else’s financial outcomes.

You have a phone, a credit score, a bank account, and limited free time.

Suggested Sources

I. . The System Change: What Shifted Between 2017 and 2023

On Hospital Capacity and the Post-Pandemic Squeeze: Needleman, J., et al. (2024): “Health Care Staffing Shortages and Potential National Hospital Bed Shortage” JAMA Network Open.

On the Nursing Exodus: National Council of State Boards of Nursing (2023): “NCSBN Research Projects Significant Nursing Workforce Shortages and Crisis”

On Hospital Financial Pressure: Advisory Board (2025): “Charted: The Current State of Hospital Finances”

II. The Algorithmic Turn: AI in Claims and Coding

On AI-Driven Prior Authorization Denials: American Medical Association (2025): “How AI Is Leading to More Prior Authorization Denials”

On Claim Denial Rates Over Time: Kaiser Family Foundation (2024): “Claims Denials and Appeals in ACA Marketplace Plans”

On UnitedHealthcare’s Algorithmic Transformation: U.S. Senate Permanent Subcommittee on Investigations (2024): “Denial of Care: How Medicare Advantage Insurers Delay and Deny Medically Necessary Care”

III. The Dashboard Problem: Why CPI Misses the Experience

On CPI Methodology for Health Insurance: Bureau of Labor Statistics (2024): “Measuring Total-Premium Inflation for Health Insurance in the CPI”

On What Medical CPI Fails to Capture: BDO (2024): “Why Medical Care CPI Falls Short in Explaining Rising Healthcare Costs”

IV. The Public Sector Control Group

On the Medicare Observation Status Trap: Centers for Medicare & Medicaid Services: “Skilled Nursing Facility Care”

On Medicaid Ghost Networks: HHS Office of Inspector General (2025): “Many Medicare Advantage and Medicaid Managed Care Plans Have Limited Behavioral Health Provider Networks”

V. The Unregulated Control Group: Veterinary Medicine

On Private Equity Consolidation in Pet Care: U.S. Senate (2024). Warren, E. & Blumenthal, R: “Investigation into Mars’ Impact on Pet Owners and Veterinary Workers”

On the Veterinary Staffing Crisis: American Veterinary Medical Association (2021): “Are We in a Veterinary Workforce Crisis?”

VI. Source Notes

On Revenue Cycle Excellence as Industry Achievement: Healthcare Financial Management Association (2023): “15 Winners Receive the 2023 MAP Award for High Performance in Revenue Cycle”

Note on the ICD-10 Transition: The 2015 shift from ICD-9 to ICD-10 expanded billing codes from roughly 14,000 to over 68,000. This is well-documented by CMS in “Transitioning to ICD-10.” The explosion in coding granularity is the structural precondition for the Revenue Cycle Management arms race described in the essay.

KFF / U.S. Census Bureau (2023): Uninsured rate reached a historic low of 7.7% in 2023. KFF Health Insurance Coverage survey; U.S. Census Bureau, “Health Insurance Coverage in the United States: 2023.”

Healthcare CPI 5-year rolling average: National Council on Compensation Insurance, “Medical Price Index” (2024); Bureau of Labor Statistics, CPI Medical Care series.

National Council of State Boards of Nursing (2023): “NCSBN Research Projects Significant Nursing Workforce Shortages and Crisis.”

KFF Health News (March 2025): “They Won’t Help Me: Patients With Private Insurance Struggle to Get Care as Insurers Deny, Delay, Restrict.” kffhealthnews.org

KFF Health News / Washington Post (December 19, 2024): “Surprise Bill: Colonoscopy at Chicago’s Northwestern Memorial” by Harris Meyer. Bill of the Month series. kffhealthnews.org

Bureau of Labor Statistics (2024): “Measuring Total-Premium Inflation for Health Insurance in the CPI.” In 2023, the CPI reported health insurance prices falling ~4% due to a methodology change in how retained earnings are measured — not a reduction in actual premium costs.

KFF Health News / NPR (December 28, 2018): “Insured But Still in Debt: 5 Jobs, Pulling in $100K a Year, No Match for Medical Bills.” kffhealthnews.org

KFF (2022): “Health Care Debt in the United States: The Broad Consequences of Medical and Dental Bills.” 41% of U.S. adults carry medical debt; total estimated at $88 billion.

KFF Health News (March 30, 2020): "Patients Appeal Observation Status Decisions After Court Ruling" by Susan Jaffe. Ervin Kanefsky case. kffhealthnews.org

CBS News MoneyWatch (April 11, 2025): “Boutique vet clinics spruce up pet care with Prosecco, snazzy waiting rooms and bespoke pricing.” Analisa Novak. cbsnews.com

CBS Pittsburgh / KDKA (September 20, 2021): “Pet Owners Face Long Waits, Veterinarians Deal With Burnout As Pandemic Impact Hits ER Vet Offices.” cbsnews.com/pittsburgh

The American Prospect (July 20, 2022): “Welcome to Hell” by Brian Osgood and Jarod Facundo. prospect.org. U.S. Senate (November 19, 2024): Warren, E. & Blumenthal, R.: “Investigation into Mars’ Impact on Pet Owners and Veterinary Workers.” warren.senate.gov

KFF Health News / NBC News (June and November 2025): “Prior Authorization Denials: Patients Run Out of Options.” Eric Tennant died September 17, 2025. kffhealthnews.org

I'm in March, reading your posts backwards and there's a clear theme emerging here: Handing over social needs (housing, healthcare, wage security, online sanity) to a financial system that doesn't care about social needs was never a good idea.

we can unpick all the reasons it doesn't work under a microscope, but the eco-socialists, and wellbeing economists have it right, as far as I can see. Neoliberalism failed.

Thank you for describing what I’m seeing and feeling. Have there been any recent changes have helped give regular people a bit more transparency into costs or bargaining power?