Waterline

The Last Supper

In 1993, Defense Secretary Les Aspin invited the chief executives of the major American defense contractors to dinner at the Pentagon. Norman Augustine of Martin Marietta was there. Executives from Lockheed, Northrop, General Dynamics, Hughes, Loral. The message from Aspin was direct: the Cold War was over, defense budgets were falling, and the federal government could not sustain the existing number of prime contractors. Consolidate or lose your contracts.

The dinner became known as the Last Supper. Over the next decade, fifty major defense contractors consolidated into five.1

The Soviet Union was gone. The peace dividend was real: resources that had been locked up for forty years in weapons programs, military bases, and defense procurement could finally flow into something more useful. The national debt was a genuine concern. The people who warned that consolidation would hollow out America’s defense industrial base sounded like Cold War fuddy-duddies who couldn’t accept that the world had changed.

Norman Augustine, who became Lockheed Martin’s CEO after the merger, offered the governing logic: comparative advantage. Let others build what they could build cheaper. The United States would focus on high-value, high-technology work. The market would handle the rest.

But a decade before the Last Supper, a quieter decision had already started that process at the waterline.

Since the 1930s, the federal government had paid what were called Construction Differential Subsidies.2 These were payments to American shipyards that offset the difference between what it cost to build a ship in the United States and what it cost to build the same ship in South Korea or Japan. American labor cost more. The subsidies closed the gap, kept the yards competitive for commercial orders, and kept the workforce alive.

By the late 1970s, the logic behind the subsidies was eroding. Korean and Japanese yards weren’t just cheaper. They were genuinely more operationally efficient. They had modernized, scaled, and invested in ways American yards had not. An analyst at the Office of Management and Budget could look at the CDS line item and make a rational case: we are paying billions of dollars per year so that American companies can build ships at three times the market price. The market can provide ships. We need to have them but someone else can build them.

In 1982, the Reagan administration cut the Construction Differential Subsidies entirely.3 The yard would still have domestic shipping contracts since American law required that goods moving between American ports travel on American-built ships. The Korean discount didn’t apply there. The yards would survive.

By 1985, commercial orders for American ships went to zero. Forty thousand shipbuilding jobs disappeared over the course of the decade.4 The yards that survived did so by pivoting entirely to Navy contracts. Bath Iron Works in Maine delivered its last commercial ship in 1984. Newport News stopped commercial work in 1999. The Philadelphia Naval Shipyard, which had employed 40,000 workers at its World War II peak, closed entirely in 1996.5

The argument for cutting the shipbuilding subsidies in 1982 was that the money would flow somewhere more productive. It did. The American economy grew. Consumer goods got cheaper. Electronics, clothing, furniture, appliances — the price of almost everything manufactured fell over the following decades, because almost everything manufactured now came from somewhere with lower labor costs, moved on ships that someone else built.

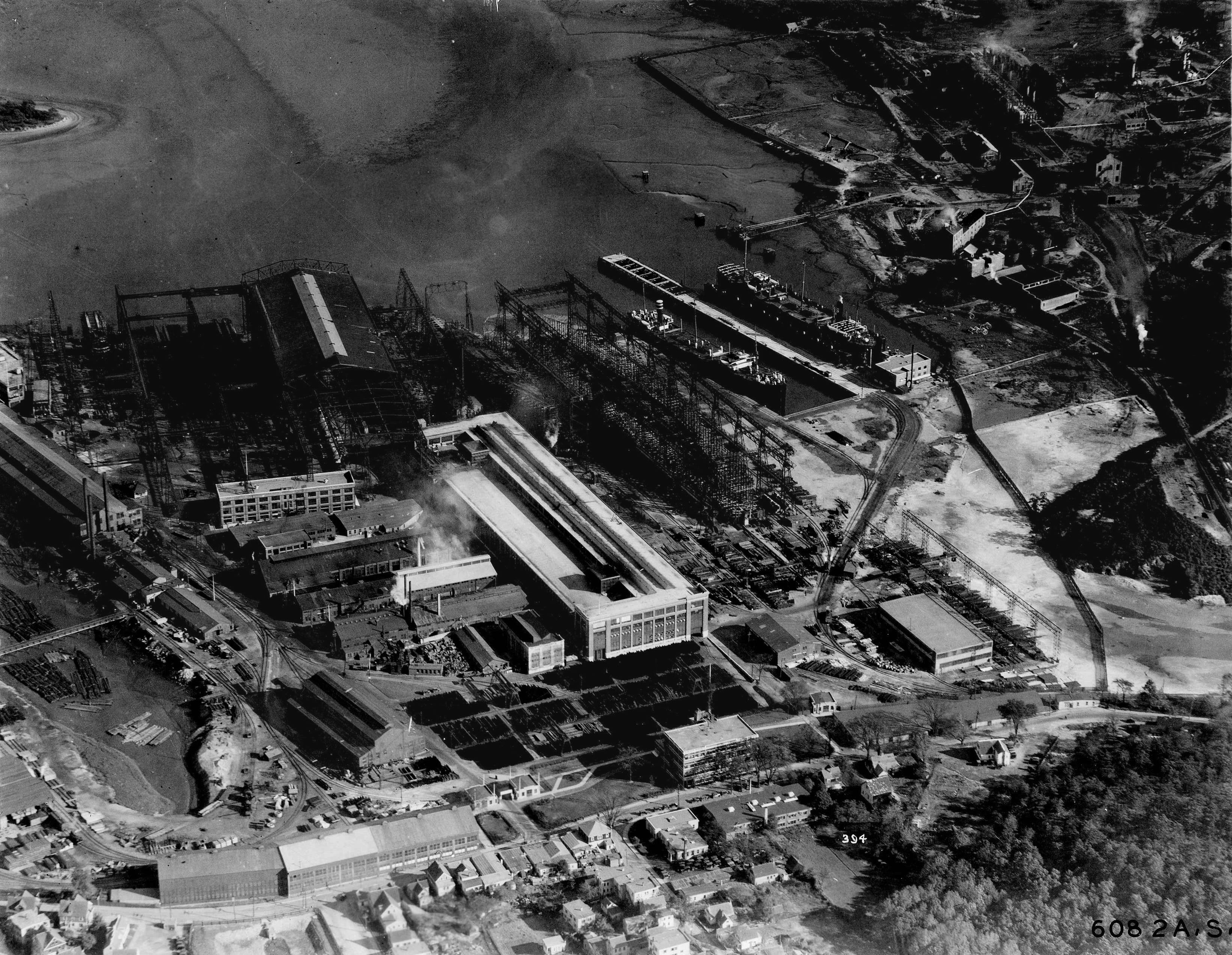

Fore River

Al Miranda had worked the Fore River yard in Quincy, Massachusetts for twenty-one years. His father had worked it for thirty-seven. The yard had employed 32,000 workers during the Second World War, 9,200 in 1967, and fewer than 1,000 when Miranda walked through it in the spring of 1986.

It closed for good that June.

“You’re not going to hear that whistle too many more times,” Miranda told a reporter that May. He was fifty-nine years old, a machinist, earning $11.53 an hour, the equivalent of about $33 in 2024 dollars.6 He had been there long enough to remember when the yard was a place men sent their sons.

“The thing is, at 59 or 55, where do you go from here,” he said. “How can you put into words what’s happening around here? I don’t know.”7

Ring-Fence

The OMB analyst was right about the immediate math. The subsidies were a cost. What the spreadsheet missed was what the subsidies were actually buying: a workforce that knew how to build ships. The welders, the pipefitters, the marine engineers, the supervisors who carried the knowledge in their hands and passed it to apprentices who became journeymen who became supervisors in turn. They were buying the yards that kept that workforce together between contracts. They were buying the trained labor pool that naval shipbuilding drew from when it needed to scale.

The assumption embedded in the 1982 decision, and again in the Last Supper in 1993, was that you could ring-fence the strategic stuff. Commercial shipbuilding could be sacrificed to the market. Naval shipbuilding was different: different customers, different contracts, different ships. The Navy would keep its yards. The workforce would be fine.

But the welders who built destroyers had learned their trade building container ships and bulk carriers and oil tankers. The pipefitters who worked on nuclear submarines had come up through yards doing commercial repair work. The supervisors who managed complex naval construction had built that expertise on commercial volume. When commercial shipbuilding collapsed, the apprenticeship pipeline collapsed with it. The yards that remained were drawing from a shrinking pool of workers who were aging out with no one behind them.

The OMB spreadsheet had no line item for this. A workforce accumulates over decades and disperses in years. When it disperses, the knowledge goes with it. It doesn’t sit in a manual. It moves through apprenticeship — through the particular understanding of how a weld behaves under pressure, how steel moves when you heat it wrong, what a finished joint is supposed to feel like — that you cannot learn by reading about it or watching a video or responding to a Navy recruiting ad during March Madness.

Twelve Years

In 2020, the Navy selected Fincantieri’s yard in Marinette, Wisconsin to build the new Constellation-class frigate. Twenty ships. The lead ship was to be delivered in 2026.8

The keel was laid on April 12, 2024.

The program was already three years behind schedule when the keel went down. The Constellation was meant to be adapted from an existing Italian frigate design, 85% commonality. Somewhere in the requirements process, that number fell below 15%. But Vice Admiral James Downey, who runs the Naval Sea Systems Command, explained the real problem at a media roundtable that spring: the yard could not hold workers. The Navy had given Marinette $50 million in retention bonuses: cash payments to keep welders and pipefitters from leaving for jobs elsewhere. The yard was building an essentially new ship, with unfinished designs, and with a workforce it could not retain.9

By November 2025, the lead ship was 12% complete. Of the twenty ships originally planned, only two will be built.10 Shelby Oakley of the Government Accountability Office put it plainly: “The Navy has no more ships today than we did in 2003.”11

While the Constellation program was collapsing, the USS Boise sat in a drydock in Norfolk. The Boise is a nuclear attack submarine. She was declared no longer dive-certified in 2017. For years, the Navy looked for a repair slot. There were no slots. In 2021, she finally entered a commercial drydock. The expected completion date is 2029.

Twelve years between “this submarine cannot dive” and “this submarine can dive again.”12

The Navy’s four government-owned shipyards are running at 130% of capacity. Destroyers take 20% to 100% longer to repair than scheduled.13

In 2021 and 2022, while the USS George Washington sat at Newport News Shipbuilding undergoing a nuclear refueling overhaul, at least seven sailors assigned to the ship died — including multiple confirmed suicides — over the course of a year. They were living aboard a vessel that resembled a construction site, in conditions that a Navy investigation found had contributed to at least one of the deaths.14

In December 2024, a South Korean defense and industrial conglomerate called Hanwha acquired the Philadelphia Shipyard for $100 million. Hanwha has announced plans to invest $5 billion rebuilding it.15

In South Korea, shipbuilding never stopped. The Korean government decided, decades ago, that shipbuilding capacity was a strategic asset worth sustaining through the lean years. It was worth subsidizing, worth protecting, worth keeping even when the market said otherwise. HD Hyundai, Samsung Heavy Industries, and Hanwha Ocean are unglamorous, low-margin, sustained businesses. But the workforce stayed. The knowledge stayed with it.

When the United States finally needed ships again, it was a Korean company buying the last American yard standing. The question Hanwha is now trying to answer is whether enough Americans still know how to help build one.

The Premium

Over the course of the World War II, American yards built more than 2,700 ships. They recruited housewives, farm workers, anyone who could learn a trade. The workers who built them had never built a ship before.

They could do it because the trades were alive. Because the yards existed. Because there was an industrial base to mobilize and train the rush of new apprentices.

In fiscal year 2023, the Navy launched a national recruiting campaign. Advertisements ran at Major League Baseball games, at NASCAR races, during UFC events. The goal: 100,000 new shipyard workers over ten years. They hired 9,700 in year one. More than half left before the end of their first year.16

Brett Seidle, the Navy’s acting acquisition executive, put the problem in sharp relief before a Senate Armed Services subcommittee in March 2025. Entry-level shipyard work now pays roughly the same as working at a gas station. “You can go down and be an attendant at Buc-ee’s for the same as an entry wage at a shipyard.”17

Al Miranda was earning the equivalent of $33 an hour in 1986, a solid middle-class wage that allowed you to support a family.

While the recruiting campaign ran, the Pentagon’s investment accounts, the budget lines that fund procurement and production capacity, fell by $13.1 billion in 2025, the first decrease in a decade.18 Defense Secretary Hegseth’s FY2026 realignment is expected to cut them further, in the latest effort to drive government efficiency.

The Trade

We made a trade.

The market provided exactly what we asked for. Demand efficiency, strip out the subsidies, and let comparative advantage run. The result was forty years of inexpensive consumer goods — electronics, clothing, appliances, furniture — manufactured in Asia and shipped to American ports on vessels built in Korean and Chinese yards. Walmart. Amazon. The standard of living that we all take as a baseline.

Those goods travel on ships. The shipping lanes through which those ships travel pass through the South China Sea.

The country whose navy patrols those lanes now builds nearly three-quarters of every new vessel on the water globally. The fleet that would need to keep them open has no more ships than it did in 2003.

The OMB analyst in 1982 was right: we didn’t need to build the ships. We needed to have them. We were just wrong about who would build them, and what that would eventually mean.

China’s shipbuilding capacity today is 232 times that of the United States.19

Suggested Sources

Arthur Herman, Freedom’s Forge: How American Business Produced Victory in World War II (Random House, 2012). The standard narrative account of American industrial mobilization in World War II — Kaiser, the Liberty Ships, what the country was capable of when it decided to be. Essential context for understanding what was lost.

C. Bradford Mitchell, Every Kind of Shipwork: A History of Todd Shipyards Corporation, 1916–1981 (Todd Shipyards Corporation, 1981). A company history of one of the yards that closed in the 1980s collapse. Granular on what the workforce and knowledge base actually looked like before the contraction.

Barry Bluestone and Bennett Harrison, The Deindustrialization of America: Plant Closings, Community Abandonment, and the Dismantling of Basic Industry (Basic Books, 1982). Published the same year Reagan’s budget eliminated the construction differential subsidies. The economic case for what happens when industrial capacity disperses — written in real time.

Ronald O’Rourke, “Navy Force Structure and Shipbuilding Plans: Background and Issues for Congress” (Congressional Research Service, updated annually). The most comprehensive public accounting of what the Navy has, what it needs, and how the gap opened. O’Rourke has tracked this for decades; the report is updated regularly and available through the CRS website.

Government Accountability Office, Navy Readiness: Actions Needed to Address Persistent Maintenance Delays, GAO-22-104765 (2022). The formal documentation of what a generation of deferred investment looks like in operational terms — submarines waiting years for repair berths, destroyers running 20 to 100 percent over maintenance schedules. Justin Katz and Jeffrey Bialos, Breaking Defense, March 2025. Two articles published two days apart that together describe the current moment: the workforce the Navy is trying to rebuild and the investment accounts being cut at the same time. Available at breakingdefense.com.

The dinner became known as the “Last Supper” in the defense industry. The consolidation that followed reduced more than fifty major prime defense contractors to five: Lockheed Martin, Boeing, Raytheon, General Dynamics, and Northrop Grumman. Barry Watts, The U.S. Defense Industrial Base: Past, Present and Future (CSBA, 2008). Daniel M. Tellep, chairman and CEO of Lockheed Corporation, became Lockheed Martin’s first chairman and CEO when the merger closed on March 15, 1995. Augustine served as president and became CEO approximately nine months later.

Construction Differential Subsidies were authorized under the Merchant Marine Act of 1936, Pub. L. 74-835, 49 Stat. 1985, which also established the U.S. Maritime Commission. The subsidies were designed to offset the difference between American and foreign construction costs and were administered by MARAD (the Maritime Administration) from 1950 onward.

Budget of the United States Government, Fiscal Year 1983 (February 8, 1982), Transportation section. The document states: “The Omnibus Budget Reconciliation Act of 1981 eliminated ship construction subsidies for 1982...No budget authority will be requested for ship construction subsidies in 1983.” Available via FRASER (Federal Reserve Archival System for Economic Research).

Shipbuilding employment declined from approximately 180,000 workers in the mid-1970s to fewer than 100,000 by the early 1990s, a loss of roughly 40,000 to 80,000 jobs depending on the baseline year used. Maritime Administration (MARAD), U.S. Shipbuilding and Repair Industry Annual Statistical Report (various years); Congressional Research Service, “U.S. Shipbuilding: The Quest to Regain Global Competitiveness” (RL32350, 2004), John Frittelli.

Bath Iron Works delivered its last commercial ship in 1984 (commercial orders had ceased in 1981) and converted entirely to Navy contracts; Newport News Shipbuilding ended commercial work in 1999. The Philadelphia Naval Shipyard, which employed more than 40,000 workers at its World War II peak and approximately 8,000 at its postwar height, was recommended for closure by the Base Realignment and Closure Commission in 1991 and closed in 1995–96, with the final Navy personnel departing in 1995 and civilian work winding down through 1996.

BLS CPI-U Inflation Calculator. $11.53 in 1986 dollars equals approximately $33.00 in 2024 dollars, a ratio of 2.86x.

“Workers Brace for Closing of Quincy Shipyard,” Los Angeles Times, May 27, 1986. All Miranda quotes and the yard employment figures (32,000 wartime peak, 9,200 in 1967, fewer than 1,000 in 1986) are from this article. Miranda’s age (59), trade (machinist), and hourly wage ($11.53) are from the same source. Archived at web.archive.org (archived August 25, 2019).

NAVSEA contract award announcement, April 30, 2020: Fincantieri Marinette Marine selected for the FFG(X) frigate program, subsequently designated the Constellation class. The contract covered up to twenty ships, with the lead ship (USS Constellation, FFG-62) originally scheduled for delivery in 2026. Reported by USNI News and Naval News, April 30, 2020.

Vice Admiral James Downey, Commander, Naval Sea Systems Command (NAVSEA), media roundtable, spring 2024. The $50 million in retention bonuses and the decline in commonality from 85 percent to below 15 percent are documented in Government Accountability Office, Navy Shipbuilding: Actions Needed to Improve Constellation-Class Frigate Program Oversight, GAO-24-106422 (2024). The keel-laying date (April 12, 2024) is public record.

The Navy cancelled the Constellation-class frigate program in November 2025. Of the twenty ships originally planned, only two — USS Constellation and USS Congress — will be completed; four contracted ships were cancelled, and the remaining fourteen were never ordered. At the time of cancellation, the lead ship USS Constellation was approximately 12% complete. Reported by USNI News, Breaking Defense, and Defense News, November 2025.

Shelby Oakley, Director of Acquisition and Sourcing Management, Government Accountability Office, testimony before Congress, 2024. The observation that the Navy has approximately the same number of ships as it did in 2003 is consistent with public Navy force structure data tracked by the Congressional Research Service. Ronald O’Rourke, “Navy Force Structure and Shipbuilding Plans: Background and Issues for Congress” (CRS, updated annually).

USS Boise (SSN-764) was declared no longer dive-certified in February 2017. The submarine spent several years awaiting a repair berth before entering commercial drydock at Norfolk Ship Repair in early 2021; the expected completion date as of 2024 is 2029. Documented in USNI News coverage of submarine maintenance backlog, 2021–2024, and in congressional testimony on Navy readiness.

Government Accountability Office, Navy Readiness: Actions Needed to Address Persistent Maintenance Delays, GAO-22-104765 (2022). The report found that the Navy’s four public shipyards — Portsmouth, Puget Sound, Norfolk, and Pearl Harbor — are operating well above planned capacity, and that destroyer and submarine maintenance periods routinely run 20 to 100 percent over scheduled duration.

Ten sailors died aboard or in connection with the USS George Washington (CVN-73) during a nuclear refueling overhaul at Newport News Shipbuilding between 2021 and 2022, including multiple confirmed suicides. Early media reporting cited at least seven suicides; the Navy’s formal command investigation confirmed the deaths and found that shipboard conditions were a contributing factor in at least one case specifically. Konstantin Toropin, “10 Deaths in 10 Months: String of Suicides on a Single Aircraft Carrier,” Military.com, April 29, 2022. The Navy’s review and its findings on conditions are documented in Pentagon reporting by NBC News, Stars and Stripes, and CNN, 2022–2023.

Hanwha Ocean acquired the Philadelphia Shipyard for $100 million in December 2024. The $5 billion investment figure is from Hanwha’s announced plans for the yard. Acquisition reported by Reuters, Defense News, and the Philadelphia Inquirer, December 2024.

Justin Katz, “Navy Struggles to Staff Shipyards Despite Recruiting Campaign,” Breaking Defense, March 26, 2025. Katz reports that 9,700 workers were hired in year one of the recruiting initiative and that first-year attrition runs 50 to 60 percent. Brett Seidle, NAVSEA’s acting acquisition executive, provided the retention figures.

Brett Seidle, testimony before the Senate Armed Services Committee Seapower Subcommittee, March 2025. The “Buc-ee’s” quote is from his prepared and oral remarks.

Jeffrey Bialos, “Continuing Resolution Cuts Defense Investment Accounts by $13.1B,” Breaking Defense, March 28, 2025. Bialos is a former Deputy Undersecretary of Defense for Industrial Affairs. The $13.1 billion figure refers to the reduction in defense investment accounts (procurement + RDT&E) under the FY2025 continuing resolution relative to the prior year’s enacted levels — the first such decrease since the sequestration era.

Alliance for American Manufacturing, based on Office of Naval Intelligence data, September 2023. The ONI estimate places China’s annual shipbuilding output at approximately 23.25 million compensated gross tons against less than 100,000 for the United States — a ratio of approximately 232 to 1. As of 2024, Chinese yards hold orders for approximately 75 percent of new vessels by tonnage. The ONI figures were subsequently reported by multiple outlets and cited in congressional testimony on naval readiness and shipbuilding capacity.