Mayday

MAYDAY — the international voice distress signal, from the French m’aidez: “help me.”

The Day the Lock Broke

On the first of May, 1975, a handful of regulators in Washington did something they believed would be a victory for fairness.

The New York Stock Exchange had been a private club since 1792, twenty-four brokers who met under a buttonwood tree on Wall Street and signed a two-sentence agreement: to trade only with one another, and to charge a fixed commission for it.1 The pledge held for a hundred and eighty-three years. Whatever you traded, a hundred shares or a hundred thousand, you paid the rate the cartel set — without haggling or discount, because no competitor was permitted to offer one. It protected lazy firms, smothered competition, and kept the market small, clubby, and unhurried.

The Chairman of the Securities and Exchange Commission ended it in a single morning. Breaking it was the right thing to do.

He was anything but a radical — a wonk, a corporate lawyer whose prior claim to fame was chairing the committee that produced something called the Model Debenture Indenture, securities arcana dense enough to put a law professor to sleep. He believed in rules, in fair play, and in the idea that breaking the cartel’s grip on price would unleash competition and modernize American finance.

“Absent any conspiracy or other artificial restraint,” he would say that fall, defending what he had done, “whatever the rates are is what they ought to be.”2

He succeeded. The brokers gave the day its name, and they meant it as a distress call: May Day — mayday — the cry of a ship going down, because going down was what they feared they were doing.3

The old aristocracy of Wall Street did die, but the Street did not. Trading costs collapsed, volume exploded, and the sleepy, relationship-bound market of mid-century America gave way to something fast, efficient, and ruthless. Today we take it for granted that we won’t pay a commission to trade stock on our phones.

That same morning, quietly, in a small office outside Philadelphia, a new company began operations, with a few dozen employees and a name borrowed from one of Nelson’s warships. It was called Vanguard.4 Nobody noticed amid the mayhem of May Day.

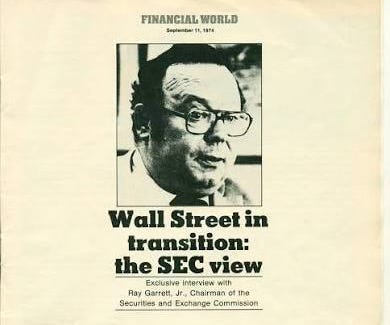

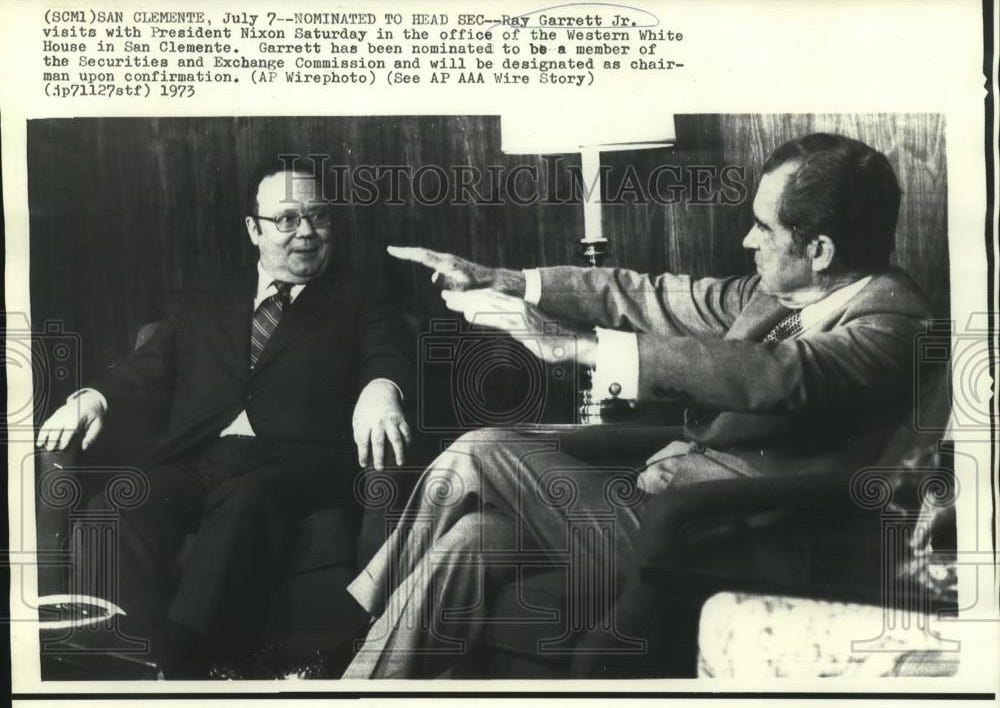

The Chairman that day was Ray Garrett, Jr. My grandfather.

I was four when he died of colon cancer, a few years after leaving the Commission. What I have of him is impressionistic — a deep, cheerful voice, and a few photographs I grew up studying. In most he is the technician of the law: horn-rimmed glasses, a sober suit, a man who found peace in the precision of a well-formed contract. His father had been a Chicago railroad lawyer, and he followed him into the law. He went to Yale, then Harvard Law, then up through the system until he was running it.

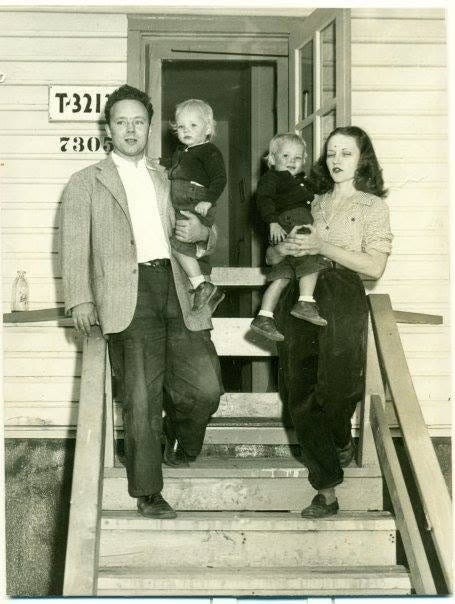

But there are other photographs. One shows him in Galveston, fresh out of basic training, next to the small-town girl he’d marry before shipping out — my Nana, from Rockdale, Texas. Another, a young artillery captain in the mud of Europe, where he fought through the Battle of the Bulge. He knew what it meant to hold a line under fire, and the worth of things that endure. Something of him endures in the Chicago he loved: to this day, Northwestern convenes an annual gathering of the securities bar in his name — the Ray Garrett Jr. Corporate and Securities Law Institute.5

His protégé Harvey Pitt — who would later hold the same chairmanship — gave me his collected speeches: the words of a man of integrity and Midwestern sensibilities, who believed, without irony, that efficiency was its own form of morality.

He was not naive about reform, either. Six weeks before May Day, he stood before the New York Chamber of Commerce and warned that the very impulse he was riding could overshoot.

“Just as revisionist history of major wars requires a generation of young historians who have no memory of the conflict,” he said, “a revisionist view of the regulatory apparatus… requires a certain lapse or absence of memory of the problems regulation was intended to solve. As the old evils fade from memory, the defects of the solution loom larger.”6

He had carried a rifle through the Ardennes. He knew what it cost to forget why something had been built. He meant it as wisdom, and it was.

May Day is the moment capital first slipped its friction, and that friction, it would turn out, had been holding something in place.

What We Owned Together

What the friction held was ownership: broad, ordinary, local ownership, on a scale most of us never learned was possible, because we were born right after it went away.

In 1945, one American household in six operated a farm. The average farmer belonged to more than one cooperative — seven and a half million memberships, more memberships than there were farms — in the mills and elevators and creameries that bought what he grew.7 In the years after the war, nearly one working American in five worked for himself: a farm, a shop, a practice, a truck.8

In 1970, thirty million Americans owned stock directly — registered by name, mailed the annual report, asked once a year for their vote. It was the high-water mark of direct ownership in American history: more than one adult in five. Three million owned AT&T alone — the widow’s stock, with roughly three owners for every employee.9

In 1975, nearly nine in ten private workers with a retirement plan held a pension — a promise the company owed them, not a balance they were left to watch.10 Nearly one in four carried a union card.11 At their height the fraternal lodges had enrolled something like one in three adult men, paying the doctor and burying the dead.12 Mutual insurers, owned by their policyholders, carried half the life insurance in the country.13 The Blue health insurers were nonprofits, organized around hospitals and physicians.

Fourteen thousand banks, most small enough to know their depositors by name, held the savings of working towns. The savings-and-loans that held the mortgages were owned by the people who saved in them.14

The reserve and the risk sat in the same hands, hands with a home in the same town, so the institution could never drift far from the human cost of its own choices.

None of it was equal, and none of it was Eden.

But the institutions that mattered had a face and a name, a meeting where neighbors argued things out, and a vote that counted.

It was ownership.

And one of the most American of truths is that people look after what is theirs.

The Melting

Then we sold it, piece by piece, across a single generation. There is a clean word for how: financialization — the slow conversion of things you held into things you traded, of stakes into claims, of membership into numbers on a screen.

The savings-and-loans converted to stock through the 1980s, and the shareholder-owned thrifts gambled their federally insured deposits until hundreds failed and the public covered the loss.15

The Blues were freed to go for-profit in 1994.16

The great mutual insurers cashed themselves in around the turn of the century — and the whole half-century of financialization can be seen in a single envelope. A Prudential policyholder opens that envelope in the spring of 2001: a letter from the board recommending yes, a disclosure of several hundred pages no one will read, and an offer — shares, or cash, for a membership in a mutual that had stood since 1875, a stake they were never taught they owned, worth a few thousand dollars. Every adviser says the same thing: it’s free money. There is nobody to argue the other side.

The members said yes, almost always, overwhelmingly.17 Nobody was robbed. They sold — a birthright most had never been taught to see as one, for a check most would spend by spring.

The farmer co-ops faced the same vise from two sides.

Gold Kist took the escape hatch: in 2004 its members voted to convert the Depression-era cooperative into a public company and cash in their shares — and within three years it had been swallowed by what became the largest chicken company on earth.

Farmland Industries, the biggest co-op in the country, with six hundred thousand member families, refused. But a cooperative cannot sell a piece of itself the way a corporation can. It can only borrow. So when Farmland’s fertilizer business cratered under the pressure of commodity swings and its debts came due in 2002, it had nowhere left to turn, and it failed outright — its pork and fertilizer arms sold to Smithfield and Koch.

Sell the stake or keep it: under the rules as written, the farmers lost their institutions either way.18

The pensions went too, except the workers never got a vote: the company simply froze the promise, closed it to everyone hired after, and handed the risk back to one new hire at a time. The mutual’s members were at least asked. The pension holder was merely informed.

Frictionless capital is a solvent. Across half a century it dissolved much of what had been built on loyalty, place, and obligation, and the economy posted historic, anomalous profits while selling off what an earlier generation had handed down.

This is the thing I have come to think of as the Great Liquidation.

Then we kept mistaking the consequences for separate problems. A healthcare problem, a housing problem, a transit problem, eventually a democracy in crisis — each with its own experts and its own column inches. But they are bills from the same sale, arriving under different letterheads. Strip the stake out of an institution and the rest follows in order: the owner who would have refused is gone, so the institution stops feeling the human cost of its own choices. The people who depend on it stop being members and become inputs. And we stop showing up for each other, because there is nothing left that is ours to show up for.

Coherence, safety, solidarity — they were what ownership quietly provided, and we sold them off without ever putting them on the receipt.

And the receipt can be totaled. For the quarter-century after the war, what workers produced and what they were paid climbed the same staircase. Around 1979 the lines diverged, output still rising, pay going flat. The gap between them, measured from 1975 to 2018, comes to roughly $50 trillion. That is on the order of $300,000 for every household it was taken from.19

A paid-off home. A down payment, a college fund, a retirement that doesn’t ride on a market’s mood.

It is America’s missing intergenerational inheritance.

And the first question any thoughtful detective would ask about a sum that large is the one question we rarely ask: where did it go?

Where It Went

There is a version of the answer we all know: it went to the top one-tenth of one percent.

And that is not exactly wrong.

The money that melted the American Dream does have owners with names. The private-equity fund that loaded the hospital with debt and sold the building out from under it. The mega-bank whose trading floor dwarfs the loans it makes to anyone who actually builds anything. The family office that files its tax avoidance under philanthropy. The foundation that studies inequality with money from an endowment invested in the causes of that same inequality.20

But do the arithmetic. Fifty years ago, in today’s dollars, the richest 0.1% of Americans held about $2 trillion. Today they hold more than $20 trillion — a tenfold rise, in real terms, captured by the same thin sliver of households at the very top.21

But 130,000 are not enough to explain the enduring politics of the past 50 years.

So where did the rest of it go?

There is about $33 trillion in the country’s retirement accounts22 that fifty years ago did not exist. The IRA was a year old. The 401(k)’s enabling clause was still unwritten. The whole edifice of modern American retirement was built from near-zero across exactly the decades the pension and the mutual and the thrift were taken apart. This is the same broad, participatory ownership, melted down and recast into an account you elect to contribute to every two weeks but do not meaningfully control.

And it is not evenly distributed. The richest 10% of households hold more than half of that money. The bottom half of the country holds about 5%.23 Nearly half of American households have no retirement account at all.

It is also old, in the plainest sense: households headed by someone fifty-five or older hold roughly 75% of all the stock-market wealth in America.

The gains of fifty years of financialization did enrich the billionaires, yes, but they also pooled, more broadly and more quietly, in roughly $300,000 lots, in tax-deferred accounts with a retirement date printed in the name.

$300,000 happens to be the missing inheritance subtracted from a hundred million paychecks. Here it is again, the same size, only now it is a balance to defend instead of a loss to grieve.24

Which is why we have never reformed financialization, only rescued it. Every time it has spun out of control the answer has always been a bailout, never a reckoning. Propose the reckoning instead, and the objection comes, gentle and reasonable, from someone who would sooner march against the rich than be caught beside them: careful, you’ll hurt people’s retirements.

They mean the 150 million of us with money in the market through our 401(k)s and IRAs. That is our trap, open for fifty years.

What Remains

But we’re nearing a moment that may disarm the trap. Because there is one thing the Great Liquidation has not yet reached.

When the farm and the shop and the mutual and the pension went, the middle class was handed a replacement and told it was an upgrade: it’s not a stake you own, but a credential you could earn.

A degree. A profession. A skill the economy would always value. You won’t own the mill anymore, but your diploma will be your mill — portable, impossible to foreclose. We stopped leaving our children the family business and started leaving them educations. We even borrowed against the house to buy them.

A whole class folded its entire hope into one scarce asset class, trained human judgment, the lawyer’s and the radiologist’s and the engineer’s and the analyst’s, and called it security.

Look at what your 401(k) actually holds, underneath the word diversified. An index fund is supposed to be the whole market: thousands of companies, the careful opposite of a bet. But it isn’t anymore.

The top ten components of the index now make up nearly two-fifths of it — a concentration past the height of the dot-com mania — and the core of that concentration is the AI-and-platform complex: Nvidia, Microsoft, Apple, Alphabet, Amazon, Broadcom, Meta, and Tesla.25

Just outside the index sits SpaceX — newly public, already valued among the giants.

The valuations holding your retirement aloft rest on one shared wager: that artificial intelligence will pay off, soon and enormously, for whoever owns the models and machines that run it. They increasingly buy one another’s chips and rent one another’s clouds and book the spending as one another’s revenue, and your account is long the entire circle.26

Your prudent, diversified, set-it-and-forget-it retirement is a concentrated bet on artificial intelligence.

So, for your retirement to climb the way it must for you to have the life the American Dream promised you, the AI bet has to win.

And the way a bet like that wins — the only way returns on that scale have ever been made — is by doing to the credential what the gig platform did to the taxi medallion: making the trained judgment of the lawyer and the radiologist and the analyst first cheaper, and then no longer the scarce, protected asset the middle class were promised we owned.

We are the ones holding that taxi medallion. The bet our retirement is riding on is a bet against the last asset our own class still owns. This is not a side effect of the Great Liquidation. It is its closing step, and we are contributing to it, every two weeks, on schedule.

The Inventory Is Gone

My grandfather put all of this in one sentence, six weeks before he pulled the lever: As the old evils fade from memory, the defects of the solution loom larger.

He thought he was warning other men — the impatient reformers, the rediscoverers of Adam Smith. He gave no sign he might be describing himself: a man so certain the cartel was the only evil that he never asked what else its friction had been holding up.

It took me a long time to stop reading that line as his, and start reading it as ours.

Which is why the rebuilding of the American Dream is more than a matter of better behavior — of selling the wrong fund, shaming the right billionaire, voting the conscience your retirement portfolio quietly overrules.

You cannot behave your way out of a trap built into the structure of what you own.

You can only own something else.

And something else means a stake you actually hold — one that pays you and answers to you, that no one can sell out from under you because you are the one holding it. Put it back into the hands of the people who carry the risk, and the next person who comes to liquidate what they depend on will find, at last, someone standing in the doorway.

The brokers were right that May Day was a distress call. But they were wrong about who was sending it. The ship going down was never Wall Street — Wall Street has never been richer. It was the slow, owned, loyal country, sold one stake at a time and converted, in the end, into the very account you are now afraid to lose.

The call went out on the first of May, 1975, in a language no one was listening for. M’aidez. Help me. It has taken fifty years to make out the words — and the hardest part of answering them is that the call is also coming from us.

Our next work is to answer it.

Further Reading

On the Great Liquidation as drift rather than a conspiracy

Greta Krippner, Capitalizing on Crisis (2011): financialization as a sequence of locally defensible choices.

On a financialized retirement account as the final form of this conversion

Gerald F. Davis, Managed by the Markets (2009).

On May Day and the SEC

Joel Seligman, The Transformation of Wall Street.

On why mutuals exist and what demutualization costs

Henry Hansmann, The Ownership of Enterprise (1996).

On the shift from pension to 401(k)

Jacob S. Hacker, The Great Risk Shift (2006).

On owning everything and deciding nothing

John Coates, The Problem of Twelve (2023); Lucian Bebchuk & Scott Hirst, “The Specter of the Giant Three,” Boston University Law Review (2019); John C. Bogle, “Bogle Sounds a Warning on Index Funds,” Wall Street Journal (Nov. 29, 2018).

On the toolkit offering exit and voice, but never a stake

Albert O. Hirschman, Exit, Voice, and Loyalty (1970).

On the 1970s mood and the bipartisan turn

Jefferson Cowie, Stayin’ Alive (2010); Gary Gerstle, The Rise and Fall of the Neoliberal Order (2022); Binyamin Appelbaum, The Economists’ Hour (2019).

The Buttonwood Agreement, signed May 17, 1792. The tree was an American sycamore — the kind early New Yorkers called a buttonwood. The first of its two sentences fixed a minimum commission; the second was a witness clause. That was the whole of the document beneath the New York Stock Exchange.

Ray Garrett, Jr., “Future Securities Markets — Reform, Not Revolution,” address to the North American Securities Administrators Conference, Mackinac Island, Michigan, September 8, 1975. The title is his, not mine. He believed it was a reform. This essay is about how his reform became a revolution.

“May Day” was the brokers’ own coinage, and a protest: the date, the sinking-ship distress call, and — for the first-of-May workers’ holiday — a jab that the SEC was importing something Russian into American finance (see Jason Zweig, “How May Day Remade Wall Street”). The name stuck instantly: my grandfather’s own address fifteen days later is titled “May Day Plus Fifteen.” The collapse came lopsidedly — institutional rates fell sharply within months while retail rates briefly rose, until the discount brokers, born that same season, arrived to serve the rest of us.

Vanguard’s management contracts took effect and the company began operations on May 1, 1975 — the same day fixed commissions died. Bogle dated the founding to the prior September; the coincidence of the operational date with May Day is noted in, among others, Jason Zweig, “How May Day Remade Wall Street.” I am not arguing the coincidence carried intent — only that history sometimes files its paperwork neatly.

Biographical details from his Washington Post obituary (”Ray Garrett Jr., 59, Dies, Former SEC Chairman,” February 5, 1980), the SEC’s historical records, and the family’s papers. The Ray Garrett Jr. Corporate and Securities Law Institute at the Northwestern Pritzker School of Law, still convenes annually — billed as the preeminent corporate- and securities-law conference in the Midwest, drawing SEC officials and Delaware judges.

Ray Garrett, Jr., “The Markets: Nationalization or Centralization?”, address to the New York Chamber of Commerce and Industry, March 20, 1975. Six weeks later the commission rule he had championed took effect. Two lines after the passage quoted, he jokes that “nothing helps nostalgia like a good wine and a bad memory,” and declines to accuse the rediscoverers of Adam Smith of bad faith — the grace this essay tries to extend him in turn.

5.86 million farms (USDA) against roughly 37.7 million households (Census Bureau historical series) — about one in six; today, 1.88 million farms among 132 million households, about one in seventy. The cooperative count is USDA, Statistics of Farmers’ Cooperatives, 1955–56: 7,730,710 marketing and farm-supply memberships against roughly 4.8 million farms. Memberships in 2022: 1.84 million, fewer now than there are farms.

Bureau of Labor Statistics: self-employment (including agriculture) was 18% of total employment in 1948; unincorporated self-employment is about 5.8% today. Proprietors’ income was 16% of national income in 1948 (BEA); the modern share is roughly half that and increasingly concentrated in professional and financial partnerships at the top (Smith, Yagan, Zidar & Zwick, “Capitalists in the Twenty-First Century,” QJE, 2019).

NYSE shareownership censuses: 30.8 million individual shareowners in 1970, just over 15% of the population — the all-time peak of direct ownership (”Stockownership in the United States,” Survey of Current Business, 1974). AT&T’s roughly three million holders are documented in the Federal Communications Law Journal. More households hold stock today, often through funds and almost always unvoted. The breadth survived but the name, the meeting, and the proxy did not.

Department of Labor, Private Pension Plan Bulletin Historical Tables. In 1975 the defined-benefit pension was the dominant form: roughly 88% of private-sector workers covered by a retirement plan were in a DB plan. (Active-participant counts — about 27.2 million in DB plans, 11.2 million in DC — overlap, since many workers held both, and so do not sum to the covered total.) The ratio has since inverted.

Bureau of Labor Statistics: roughly one in four wage-and-salary workers carried a union card in the mid-1970s; 9.9% in 2024, and 5.9% in the private sector.

David T. Beito, From Mutual Aid to the Welfare State: Fraternal Societies and Social Services, 1890–1967 (UNC Press, 2000). The one-in-three estimate is for adult men circa 1920; the lodges paid sickness and burial benefits and often retained a doctor on contract for members.

Mutual life insurers held roughly half of U.S. life-insurance-industry assets at mid-century. See J. David Cummins and Krupa Viswanathan, “Ownership Structure Changes in the Insurance Industry: An Analysis of Demutualization,” Journal of Risk and Insurance, 2003.

FDIC: 14,483 insured commercial banks at the 1984 peak; about 4,000 today. Roughly 4,000 savings-and-loans in 1980; about 550 thrifts remain.

The mechanism ran in that order. The Garn–St. Germain Act of 1982 eased mutual-to-stock conversion and, in the same stroke, widened what thrifts could speculate in — against deposits freshly insured to $100,000, the textbook recipe for gambling with someone else’s money. Cleanup cost the public about $124 billion (FDIC). The tell is the natural experiment in the wreckage: research at the Federal Reserve Bank of Kansas City (Padma Sharma) found that stock-form S&Ls took on far more risk than the depositor-owned mutuals beside them, which declined to gamble even when the insurance made losing free. When you strip the stake, a thrift becomes a casino.

The Blue Cross Blue Shield Association changed its rules in 1994 to permit member plans to convert to for-profit status.

The great mutual life insurers demutualized in a wave around 2000–2001 — Mutual of New York, John Hancock, MetLife, Prudential. On the votes, I will not pretend the record is tidy: approval among ballots cast typically ran well past two-thirds and often past 90%, but turnout was low and the disclosure documents were written to never be read. Whether a vote like that constitutes consent is a fair question. It was, in any case, a yes.

Gold Kist’s members voted to convert in 2004; the shares priced at $11, and in January 2007 Pilgrim’s Pride bought the company at $21 in cash, creating the world’s largest chicken producer. Farmland’s was the other kind of death. A cooperative cannot raise outside equity — that constraint is what keeps it member-owned — so its only external capital is debt, and it must buy members’ equity back as well. After a decade of debt-financed expansion, when its natural-gas-dependent fertilizer business lost $87 million in a single quarter, Farmland could no longer roll over $570 million in maturing obligations. It filed Chapter 11 in May 2002 with $1.9 billion in debt. Its private rivals (Cargill, Koch) carried permanent equity and fortress credit ratings. Its public rivals could simply issue stock. A co-op could do neither.

Carter C. Price and Kathryn A. Edwards, “Trends in Income From 1975 to 2018,” RAND Corporation, 2020. The aggregate is approximately $47 trillion, commonly rounded to $50 trillion. The underlying flow is about $2.5 trillion in 2018 alone. The cumulative per-household figure is back-of-envelope and denominator-sensitive — spread across U.S. households it runs on the order of $300,000, higher if confined to the bottom 90%. Strictly the figure is a flow — cumulative income the bottom 90% never received — but the essay reads it as the wealth that income would have become: the home equity, the savings, the inheritance that never formed. Treat it as scale, not an invoice. Where the wedge went is its own literature: Federal Reserve economist Michael Smolyansky found that more than 40% of real corporate profit growth from 1989 to 2019 came not from better companies but from falling interest rates and falling corporate tax rates (”End of an Era,” Federal Reserve FEDS series, 2023). The wages that went flat and the margins that went up were one income statement.

This is its own argument, made most forcefully from outside these pages: see Delta Fund, “You Built This”, on how foundation and family-office capital underwrites the extraction those same institutions deplore. The Ford Foundation committed $1 billion to mission-related investing against roughly $12 billion in conventional vehicles; the gap is the argument.

The figures are read here as wealth (a stock), so the comparison stays apples-to-apples. The capture shows up two ways. As a share: the top 0.1%’s slice of all U.S. wealth roughly tripled, from ~7% in the mid-1970s (the modern low point) to ~18–20% now — the Saez–Zucman series (capitalized-income method; World Inequality Database / Realtime Inequality; survey-based SCF/Wolff measures run lower, nearer 14% today, and the Fed’s Distributional Financial Accounts do not break out the 0.1% at all). In real dollars, the text’s numbers are a transparent derivation, not a single cited figure: that share against Federal Reserve total household net worth (~$6 trillion in the mid-1970s, roughly $180 trillion today), inflation-adjusted, gives roughly $2 trillion then (today’s dollars) and ~$25–35 trillion now — a real increase on the order of tenfold. The tenfold growth and the tripling of the share are the robust claims; the exact dollar endpoints are estimates that depend on which series you use.

Defined-contribution plans (401(k)-type) and IRAs together hold roughly $33 trillion (Investment Company Institute). Strictly 401(k)s plus IRAs are nearer $29 trillion; the rest is 403(b)s, 457s, and similar accounts. Counting the surviving defined-benefit pensions, total U.S. retirement assets run to about $48 trillion. The pool is a creature of these same fifty years: the IRA was created by ERISA in 1974, the 401(k)’s enabling clause added by the Revenue Act of 1978 (the first plans appeared around 1981) — so a half-century ago it was, to a rounding error, zero.

The accounts are concentrated twice over. Per the Congressional Research Service (analysis of the 2022 Survey of Consumer Finances), 45.7% of U.S. households held no retirement account at all. Of defined-contribution assets the top 10% of households hold roughly 55% and the bottom half about 5% (Federal Reserve, Distributional Financial Accounts); households 55 and older hold roughly 75% of all household stock-market wealth (same source, by age). The flip side of that 45.7% is breadth: a small majority of households — on the order of 150 million individual Americans — hold some retirement money, which is exactly what makes “you’ll hurt people’s retirements” such durable politics even as the value concentrates at the top.

Among households earning $150,000 or more, the median retirement-account balance was about $316,000 and the average $729,866 (Congressional Research Service, “Ownership of Retirement Accounts in 2022”). That this is the same order of magnitude as the missing inheritance of the previous section — roughly $300,000 a household — is the argument, not a coincidence. Read both as wealth: the inheritance that never formed at the bottom, and the balance that did form nearer the top. They are not the same dollars in one ledger, but they are the two ends of a single redistribution — the wages that stopped rising widened the margins, the margins were priced into the stock, and the stock was swept into the accounts of the households the wage cut spared.

The top ten components of the S&P 500 make up nearly two-fifths of the index by value — past the peak of the 1999–2000 technology bubble (Capital Group; Columbia Threadneedle, 2026). The eight named in the text are the AI-and-platform core of that concentration, not a strict list of the top ten by weight — exact membership shifts with daily prices and with how Alphabet’s two share classes are counted. Tesla belongs because by 2026 it is valued not as a carmaker but as an AI-and-robotics bet — autonomy, the robotaxi, the Optimus humanoid. SpaceX — larger than Tesla after its June 2026 IPO, the largest in history, and likewise pitched as an AI-and-connectivity play — is not yet in the S&P 500 (it posted a 2025 loss and has not met the index’s seasoning requirements), so it is named separately, not among the eight; counting it, the largest nine are worth roughly $28 trillion. Index weights move constantly.

The AI buildout is no longer funded only out of retained earnings. Across the hyperscaler complex the boom has pulled in corporate debt, lease obligations, project finance, and circular vendor commitments — the balance-sheet machinery of a capital cycle, not just the cash spending of unusually profitable firms. Some sits on the companies’ own books (Meta’s long-term debt rose to roughly $59 billion by the end of 2025; Amazon’s to about $66 billion, with lease liabilities higher still), much sits off them (leases, special-purpose vehicles, partner and vendor financing), and an estimated $120-billion-plus in new debt was issued across the major players in 2025 alone (per Mellon and Reuters reporting). I am not predicting a crash. The point does not require one. The specific figures move but the direction does not.

"As the old evils fade from memory, the defects of the solution loom larger."

- Ray Garrett, Jr.

Well written, great perspective. Thank you for sharing, Evan.

I never did trust my pension.